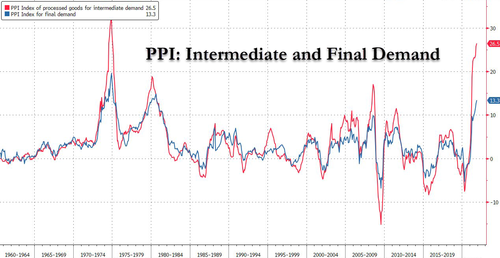

The Federal Reserve’s last meeting of the year is also probably the most anticipated, and could bring a hawkish tone after Tuesday’s record producer price data confirmed that inflationary pressures will feed through into next year as pipeline inflation remains scorching hot as final demand PPI has a long way to go before it catches up to intermediate demand.

While we have already done two FOMC preview articles (here and here), courtesy of BBG’s Ven Ram, is what the markets are expecting from policy makers on various fronts:

Taper:

This may be the easy part for the Fed. With Chair Jerome Powell having already flagged the possibility of wrapping up bond purchases “a few months earlier,” rates markets have taken the news in their stride. Consensus expects the pace of tapering to increase to $30 billion per month from $15 billion. While $25 billion is also a whisper, an increase to “only” $20 billion would be seen as dovish. Technology stocks have thrown a bit of a tantrum, yes, but that’s irrelevant for the Fed (it will become relevant if the small drop becomes a 20% plunge in the GAMMA generals). This means that next month the Fed will buy $90BN in TSYs/MBS; $60BN the next month, then $30BN before it ends purchases some time in March, which is where the market’s expectations are centered, and a significant deviation here looks unlikely. Indicatively, this is what Goldman thinks the timeline for tapering and rate hikes in 2022 will look like.

Dot plot:

The plot is likely to see a significant shift. The median for 2022 is bound to acknowledge the current market pricing for two full rate hikes. The plot for 2023 already saw three increases, and I expect it to be unchanged. A shift upward in the 2024 median, currently at 1.75%, will be a hawkish takeaway, though a change in the longer-term target rate from 2.50% looks unlikely.

Summary of economic projections:

Bloomberg Economics expects an upward revision in the headline PCE for 2022 forecast to 2.5% from 2.2%, while NatWest’s Kevin Cummins expects the revision to be even higher at 2.7%. He also expects a moderation in real GDP forecast to 3.5% from 3.8%.

Post-meeting briefing:

Powell will aim to do a careful balancing act, especially if the collective dot plot leans on the more hawkish side. He will also emphasize that we don’t know how the labor market will fare in the face of the new variant and how resilient consumer demand will be. If indeed stocks tumble after seeing the “hawkish” dot plot at 2pm, Bloomberg’s Alyce Anders suggests that Powell is likely to temper that hawkishness at the press conference. According to Anders, the curve may actually be steeper by the end of the day as entrenched flatteners unwind and call it a year. Plus, Fed tapering eliminates the marginal buyer, meaning other entities need to step up their buying. That requires a steep curve with lots of carry, traders point out.

Runoff discussion:

Among the more interesting parts of Powell’s remarks will be what the Fed intends to do with its humongous balance sheet. With St. Louis Fed President James Bullard having commented on the prospect of allowing a balance sheet runoff at the end of taper, policy makers will have likely deliberated on the issue, and the remarks will determine how the longer end of the curve reacts to the meeting.

Here’s what other investors and strategists are thinking about as Powell gets ready to step up to the lectern one last time this year:

JoAnne Feeney, partner at Advisors Capital Management:

“Powell’s chief concern will be to convince markets that the Fed has the tools to bring inflation lower and signaling a faster taper will be a key element. But he will also try to reassure investors that this move will not compromise the further recovery of production and of real economic activity, and he is likely to cite some improvement in employment and supply chain bottlenecks to support that view. The Fed needs to make sure to maintain its credibility by aggressively moving to turn the inflation trend around.”

Adam Phillips, managing director of portfolio strategy at EP Wealth Advisors:

“Investors are now focused on how the Fed will thread the needle of applying the brakes without stalling the economy. We’re just about 2% off the record high on the S&P 500, but the broad index is masking some interesting developments beneath the surface. It’s not lost on us that staples and utilities are the best-performing sectors so far in December. The fact that staples is outperforming discretionary on an equal-weighted basis also bears watching.”

Emily Roland, co-chief investment strategist at John Hancock Investment Management:

“The Fed holds the keys to this cycle. If they move quickly to stomp out inflation, they may risk cutting the cycle short. If they decide that they can be a little bit more patient — which, I think, is looking harder and harder — they have the ability to extend this cycle. We’re setting up for some hawkish moves into next year.”

Drew Matus, chief market strategist for MetLife Investment Management:

“I want to see with regards to the Fed funds rate changes — which I think the Fed is going to signal that they’re going to go more than once in 2022 — whether they signal more than that. Have we leapfrogged over the moderates? Have we gone straight into a much more hawkish stance? If we see that leapfrogging that suggests that the Fed feels like it might be a little behind the curve. That’ll make people nervous and move them into more of a risk-off framework.”

Kevin Gordon, senior investment research specialist at Charles Schwab:

“The notion that the market’s been resilient this year hasn’t been fully true — what you just have to do is peel it back one layer and you can see that. We’re approaching a really crucial point. It’s probably not going to be as clear until we get more clarity on the inflation picture, heading into the first quarter and then into the second quarter.”

Brian Nick, chief investment strategist at Nuveen:

“The risk of the Fed tightening — which gets more severe every time we get a high inflation number, like the producer prices we got this morning — and then omicron, which is completely independent, those two things are wreaking havoc day to day with the market. But it’s been impressive to see that we were, as of Friday, back to all-time highs. We’re not that far off — so there’s still a lot of resilience, there’s still a sense of investors still aren’t sure where to go if it’s not U.S. large cap.”

Finally, here is what Goldman expects the Fed’s statement redline comparison to the last FOMC meeting will look like:

And here is Morgan Stanley’s redline:

{kind=link}